AI Risk Observatory:

Tracking AI Risk and

Adoption in UK Public-

Company Annual Reports

Executive Summary

Context and motivation. Artificial intelligence is reshaping the risk and operational landscape of UK listed companies at a rapid pace. Annual reports, as legally mandated, board-accountable, and audited artefacts, represent a systematic evidence base for tracking how companies understand, disclose, and govern their AI exposure. The AI Risk Observatory applies a reproducible, large-language-model-based classification pipeline to the full population of UK listed companies to produce, for the first time, a structured and longitudinal analysis of AI disclosures, for all listed companies on the London Stock Exchange and the Aquis Exchange.

What we studied. As at the report date, the corpus covers 9,821 annual reports from 1,362 companies, spanning publication years 2020 to 2026 (2026 partial). Across these we analysed the mentions of AI adoption, risk, harms, and vendors of AI technology. The classification pipeline was calibrated against a human judge, and achieved a higher accuracy than the initial human-annotated review. The annual reports were sourced from FinancialReports.eu and Companies House. Each report is processed through a two-stage classification pipeline using Gemini Flash 3 as the production model.

(up from 19.8% in 2020)

2020 → 2025

Core Findings. First, AI mentions in annual reports have grown rapidly. In 2020, 19.8% of reports contained any AI mention; by 2025 that figure reached 65.5%. Risk-specific mentions grew even faster from a much smaller base, rising from 2.8% of reports in 2020 to 41.2% in 2025. In count terms, annual reports mentioning AI risk increased from 28 to 643, a twenty-three-fold increase. The sharpest single-year increase occurred between 2023 and 2024 (370 more AI risk mentions), coinciding with mass-market generative AI adoption.

Second, disclosure quality has not kept pace with disclosure volume, and the weakness is sharpest in risk reporting. Our substantiveness classification (a measure of how elaborate a statement is), shows that in 2025, only 10.4% of AI risk mentions were classified as substantive, compared to 33.8% of AI adoption mentions that year. The dominant pattern is moderate disclosure: companies increasingly identify AI-related uses, risks, and providers, but usually without the mechanisms, controls, deployment detail, metrics, or timelines needed for decision-useful reporting.

Third, there are significant differences between sectors and between market segments (LSE Main Market vs AIM). Finance and Health CNI sectors have high levels of relevant AI mentions while Data Infrastructure and Energy show thin disclosure relative to their plausible operational AI exposure. FTSE 100 companies mention AI substantially more than the rest of the studied companies (84.8% AI mention rate, 68.6% risk rate in 2025), while AIM companies' reports mention AI significantly less (36.8% signal rate, 6.4% risk rate). Vendor concentration is a factor that is the hardest for us to analyse: Microsoft remains the leading named provider, but 36.0% of AI provider references in 2025 were either undisclosed or referred to a third party outside the main named-provider buckets, which may mask growing infrastructure dependencies on a small number of hyperscalers.

1. Introduction

1.1 Motivation

We study annual reports because they are legally mandated, board-accountable documents under the Companies Act and the FCA's Disclosure Guidance and Transparency Rules. They provide a large, sector-spanning dataset with a natural time series. Crucially, these reports are produced within a legal accountability framework that creates strong incentives for accuracy and follows a relatively stable year-to-year process, unlike more variable sources such as executive media appearances. This makes them particularly well suited, compared with surveys or press releases, for tracking how companies understand and govern their AI exposure.

The main legal basis for narrative risk reporting sits in the Companies Act 2006. For companies required to prepare a strategic report, the report must include a fair review of the business and "a description of the principal risks and uncertainties facing the company" (ss. 414A–414C, subject to the small companies exemption in s. 414B). FRC guidance indicates that these disclosures should be company-specific and sufficiently specific for shareholders to understand why they matter to that company; where a risk is more generic, the description should explain how it affects the company specifically.1 At the market-disclosure layer, the FCA's Disclosure Guidance and Transparency Rules (DTR) 4.1 require issuers to publish annual financial reports within four months of the financial year end. AIM companies, governed primarily by the London Stock Exchange's AIM Rules for Companies, have a six-month deadline for annual audited accounts under Rule 19 and a more flexible governance-disclosure regime under Rule 26. That lighter AIM framework may help explain part of the disclosure gap identified in the findings, alongside differences in size, resources, and exposure.

By creating a data processing pipeline that automatically scans 9,821 annual reports from 1,362 UK-listed companies spanning publication years 2020 to 2026, we can identify, categorise, and quality-rate AI-related disclosures, producing structured signals across adoption type, risk category, vendor dependency, and disclosure substantiveness. This allows us to establish a replicable, longitudinal baseline intended to be useful for policy, supervisory prioritisation, and research on the evolution of corporate AI governance in the United Kingdom's Critical National Infrastructure (CNI). Our focus on CNI is motivated by the shared interests of our funder, the societal resilience team at the UK AISI.

1.2 Research Questions

This project began with three foundational questions:

- Can large language models reliably extract structured AI-related signals from unstructured annual report text at scale? The answer, validated through our methodology, is yes: LLM-based classification produces consistent, auditable results across a corpus of this size.

- Does applying this method to UK listed companies yield statistically significant or otherwise noteworthy findings? Again yes: the patterns we observe in disclosure rates, substantiveness, and sector distribution are sufficiently robust to warrant attention.

- Is this kind of data useful to AISI or to policymakers more broadly? We believe it is, and the findings presented here are intended to support that case, though we are still actively working to determine the most effective ways to make this data actionable for regulators and policy teams.

With those questions in view, this report organises our empirical findings around four themes.

First, how has the prevalence of AI-related disclosure changed across UK listed companies between 2020 and 2025? This encompasses the growth in the share of companies disclosing anything about AI.

Second, in what way is AI mentioned in these reports? With the primary focus on the reported risks from AI, levels of sophistication or types of AI adoption, and the AI technology vendors.

Third, are the AI disclosures substantive rather than boilerplate? The concern here is not merely whether companies mention AI risk (they increasingly do), but whether those mentions contain the specific operational detail, named systems, and governance evidence that would make them informative to investors, regulators, and researchers. A disclosure regime in which mention rates grow while quality stagnates is formally responsive but substantively hollow.

Fourth, what are the differences in the AI mentions across CNI sectors and market segments? This question is motivated by the Observatory's Critical National Infrastructure focus. The UK's CNI framework designates thirteen sectors whose failure or compromise would severely impact essential services, national security, or the functioning of the state, with potential for widespread and cascading consequences across interconnected sectors. These include: Energy, Finance, Transport, Health, Communications, Water, Food, Government, Defence, Civil Nuclear, Chemicals, Data Infrastructure, and Space. These sectors are defined and maintained by the National Protective Security Authority (NPSA). The CNI sectors have an undeniable AI exposure: Energy faces operational technology/information technology (OT/IT) convergence risks; Finance relies on AI for trading, credit, and fraud detection; Health is deploying AI in clinical pathways; Communications mediates content at infrastructure scale. Two features make CNI disclosure monitoring particularly important: sector interdependence means AI failures can cascade across boundaries, and most CNI rely on AI from a small number of third-party providers, creating vendor concentration risk that may not be visible in public disclosures. Sectors whose disruption would have cascading national consequences may therefore present AI exposure patterns that are underrepresented in the disclosure record.

1.3 Scope and Contribution

Most large-scale empirical work on AI disclosure has focused on US markets, specifically the SEC's 10-K mandatory filing. The most comprehensive recent study, Uberti-Bona Marin et al. (2025), analyses over 30,000 US filings and finds a steep rise in AI-risk mentions alongside persistently generic content. Lang and Stice-Lawrence (2015) demonstrated that large-sample textual analysis of annual reports outside the US is both feasible and methodologically sound, but empirical coverage of UK listed companies at scale remains sparse.

This report makes four contributions. It provides the first large-scale structured analysis of AI disclosure across the full population of UK listed companies, covering both Main Market, AIM and AQSE issuers. It introduces an explicit substantiveness dimension that distinguishes boilerplate from substantive disclosures (tangible evidence of action taken by the company versus empty statements), a feature absent from most prior work in this domain. It applies a CNI-sector decomposition that connects corporate disclosure patterns to the UK's national security and infrastructure resilience frameworks. And it establishes a reproducible pipeline, using Gemini Flash 3 as the production classifier, that can be re-run regularly as the regulatory landscape evolves under the 2024 UK Corporate Governance Code.

Funding and conflicts of interest. This research was supported by the UK AI Security Institute (AISI). The majority of the annual report filings used in this research were sourced from FinancialReports, a third-party data provider specialising in structured access to public company filings in machine-readable format. FinancialReports provided access to its corpus without a monetary fee; in exchange, we agreed to credit and reference their service on the AI Risk Observatory dashboard. The authors declare no conflicts of interest that could be perceived as influencing the objectivity of this report.

The live view of the findings can be found at riskobservatory.ai.

2. Methodology

2.1 Corpus and Universe Definition

Our goal is to process all filings available from public companies in the UK. Thus our target universe is approximately 1,660 public companies listed in the UK at the time of writing. However, not all of them have annual reports that are accessible to us. To ensure consistent and reliable data, the universe was restricted to UK-incorporated entities only, removing 191 companies incorporated outside the UK (primarily in Ireland, the Netherlands, and Australia) that are LSE-listed but hold no Companies House registration. This gives us a universe of 1,469 companies across three market segments: the Main Market (including FTSE 350), AIM, and Aquis. The market segmentation of companies and reports can be seen below:

Market segment coverage

| Market Segment | Companies | Reports |

|---|---|---|

| Main Market Total | 776 | 7,827 |

| Main Market (FTSE 350) | 289 | 3,638 |

| Main Market (FTSE 100) | 85 | 1,359 |

| Main Market (FTSE 250) | 204 | 2,279 |

| AIM | 497 | 1,484 |

| Aquis Exchange | 33 | 74 |

| Not classified | 64 | 458 |

The number of listed companies on the exchanges is not constant as delistings, spin-offs and new listings happen regularly. This causes a fluctuation in the number of companies and reports in each year. Our universe includes all companies that are listed in a given year in the UK, as they have to file annual reports to Companies House.

The temporal scope covers publication years 2021 to 2025 as the primary analysis window. We collect reports based on the publication date, the calendar year in which an annual report was filed to Companies House. Reports published in 2020 and the first months of 2026 are included in the corpus but, given their incomplete coverage, should be treated as supplementary; any statistics for these two years should keep that limitation in mind.

The full target is 7,345 company-year slots (1,469 companies × 5 publication years). The final corpus contains 9,821 processed reports spanning 1,362 companies, with the difference from the target reflecting the inclusion of 2020 and partial 2026 data alongside the exclusion of 125 companies for which no processable filing was found across any year.

Each company is assigned to a CNI sector using a mapping from the International Standard Industrial Classification (ISIC) to the NPSA sector taxonomy. The mapping involves inherent ambiguity (not all ISIC codes align cleanly with CNI sector boundaries), and some companies operate across multiple sectors; where this occurs the primary classification is used. The sector distribution in the corpus reflects both the actual composition of the LSE-listed universe and the limitations of the mapping: Finance (461 companies), Energy (141), Health (111), Transport (61), Communications (28), Water (18). The mapping is described in full in Appendix B.

2.2 Data Ingestion

Annual reports were collected from two complementary sources to maximise coverage across market segments and years.

The primary source is FinancialReports.eu (FR), which aggregates annual filings submitted to Companies House and converts them to machine-readable structured markdown. FR provides strong coverage for Main Market companies, reaching approximately 95% of FTSE 350 company-year slots, but significantly weaker coverage for AIM, where it captures only around 28% of available filings. This asymmetry reflects the lighter electronic filing requirements for AIM companies rather than any gap in actual corporate reporting.

The secondary source is Companies House (CH), which holds the PDF copy of every annual report filed by UK-incorporated companies regardless of market segment. PDF filings were downloaded via the Companies House API and converted to markdown through an OCR pipeline. The CH route serves primarily as a gap-fill for companies absent from or incompletely covered by FR, primarily AIM companies. Cross-year deduplication was applied to remove documents appearing in adjacent publication years that were, in fact, the same document. This double-counting mainly arose from files with publication dates spanning December and the following January: one data source (FR) recorded the earlier date, while the other (Companies House) used the later one.

Despite combining both sources, 178 companies with confirmed Companies House filings could not be matched to any FR annual report, due to ingestion or classification failures on the FR side. The clearest case is Jet2 PLC, where FR entries labelled "Annual Report" were in fact share buyback notices; the actual annual report was absent from FR's index entirely. These gaps are partially mitigated by the CH PDF route but are not fully resolved. Coverage detail and CNI mapping are summarised in Appendix B.

2.3 Preprocessing

We normalise the markdown versions of the annual reports, whether from FR or Companies House, to a consistent plain-text format with section metadata retained. The normalisation step strips all preprocessing artefacts while preserving structural signals such as headings and section boundaries. The headings and section boundaries serve as useful metadata for the processing of AI mentions.

To focus processing on relevant material, a keyword gate is applied before any LLM classification. A passage must explicitly mention artificial intelligence (the list of terms used can be found in Appendix D), machine learning, large language models, generative AI, or a clearly AI-specific technique, such as neural networks, computer vision, or natural language processing, to pass the gate. Terms that commonly appear in annual reports but do not reliably signal AI, including "data analytics," "digital transformation," "automation," and "advanced analytics," are excluded unless they appear alongside an explicit AI qualifier. This conservative gate reflects a deliberate design choice: reducing false positives is prioritised over maximising recall, given that inflated mention counts would undermine the credibility of trend analysis at scale.

Passages that pass the gate are extracted with a context window of two paragraphs before and after the triggering passage, providing the classifier with enough surrounding text to assess intent and tone accurately. We ensure no duplicates are created by avoiding overlapping windows between two adjacent passages in the same document. Each resulting passage carries structured metadata: company identity, publication year, market segment, CNI sector assignment, and the report section in which the passage appeared. We refer to these passages of text that mention AI as AI mentions.

2.4 Classification Pipeline

Classification proceeds in two sequential stages applied to each AI mention.

Stage 1: Mention-type classification determines whether the chunk carries a meaningful AI signal and, if so, what kind. The classifier assigns one or more of the following labels to each AI mention (described in Table 1): adoption, risk, vendor, harm, general_ambiguous, none.

These labels are not mutually exclusive except for none, which indicates "false positives" and must appear alone. Stage 1 enforces a strict filter for false positives: adoption requires company-specific deployment language (i.e. "we deployed," "our system uses") not strategic intent or false aspiration. Risk requires AI to be attributed as the source of a downside, not merely mentioned in proximity to risk language. A passage describing risk and AI does not qualify as an AI risk disclosure unless AI is named as the risk source. All tangible mentions of AI that are not false positives and also don't fall into the four main categories (risk, adoption, harm, vendor) are classified with the general_ambiguous tag. It's worth noting here that each AI mention might consist of multiple sentences, some of which might be labelled as general_ambiguous, making this tag inherently not mutually exclusive.

Stage 2: Deep classification is applied to AI mentions that were labelled in Stage 1. We run three parallel classifiers for each of the three tags:

The adoption classifier characterises the type of AI being reported. Each chunk is scored across three non-mutually-exclusive categories: non-LLM (traditional machine learning, computer vision, predictive analytics, fraud detection, recommendation systems), LLM (large language models and generative AI tools, including named products such as ChatGPT, Gemini, and Microsoft Copilot), and agentic (autonomous AI systems that execute tasks without continuous human oversight; the key distinguishing characteristic is autonomous action, not AI-assistance). Each category receives a signal score from 0 to 3 reflecting the directness of evidence. Adoption chunks also receive a substantiveness rating based on whether the company names a concrete use case, system, scale, outcome, or operational context.

The risk classifier maps the AI-related risk to one or more of ten categories: strategic and competitive, cybersecurity, operational and technical, regulatory and compliance, reputational and ethical, third-party and supply chain, information integrity, workforce impacts, environmental impact, and national security.

The vendor classifier identifies the AI provider referenced in the chunk. Named tags cover Microsoft, Google, OpenAI, Amazon, Nvidia, Meta, Salesforce, IBM, Databricks, Snowflake, Anthropic, xAI, Palantir, ARM, Mistral, and UK AI providers; an open_source_model tag captures deployments of open-source models without a named commercial provider; an internal tag captures companies describing in-house AI development; other covers explicitly named providers not in the named list; and undisclosed is used when a company references an external AI capability without naming the provider. Vendor chunks receive a substantiveness rating based on whether the provider or model is named and linked to a concrete use case, deployment context, scale, or outcome.

Each of the three classifiers additionally assigns a signal score to each assigned tag. There are three signal scores: 1) Explicit, 2) Strong Implicit, 3) Weak Implicit. For example, the adoption classifier might tag the following AI mention: "We are implementing an AI chatbot in our customer service that can autonomously handle phone calls" as: Agentic (explicit), LLM (strong implicit), non-LLM (weak implicit). This allows us to filter how explicitly a given taxonomy label is evidenced throughout the reports.

Additionally, each AI mention is tagged with substantiveness scores as described in the Stage 2C table below.

Stage 1: Mention Types

| Label | Definition used in the classifier |

|---|---|

adoption | AI actively deployed, used, piloted, or implemented by the company or for clients. Requires company-focused language (i.e. "we/our") to avoid all general statements on AI being adopted by other parties. Intent, strategy, or roadmaps alone do not qualify. |

risk | AI described as a source of material risk or downside. AI must be attributed as the risk source; generic risk language without explicitly mentioning AI is not risk from AI. |

harm | AI described as having caused a past harm (such as: misinformation, fraud, safety incident, discrimination, etc.). |

vendor | Explicit named reference to a third-party AI provider or platform. |

general_ambiguous | AI explicitly mentioned but not meeting any of the above thresholds: high-level plans, strategic positioning, or non-specific AI references. |

none | False positive (place name, unrelated abbreviation), or automation language without explicit AI specificity. |

Stage 2a: Adoption Types

| Label | Definition |

|---|---|

non_llm | Traditional AI/ML: computer vision, predictive analytics, fraud detection, recommendation engines, anomaly detection, Robotic Process Automation (RPA) with ML components. |

llm | Large language models and generative AI: GPT, ChatGPT, Gemini, Claude, Copilot, text generation, NLP chatbots, document summarisation, code generation. Copilots and AI assistants default to this category unless explicitly described as autonomous. |

agentic | AI systems that autonomously execute tasks with limited human oversight. The defining characteristic is autonomous action: the system acts and decides independently rather than assisting a human who decides. |

Stage 2b: Risk Categories

| Category | Definition |

|---|---|

strategic_competitive | AI-driven competitive disadvantage, industry disruption, failure to adapt or adopt. |

operational_technical | AI model failures, reliability/accuracy issues, hallucinations, system errors, decision-quality degradation. |

cybersecurity | AI-enabled cyberattacks, fraud, impersonation, adversarial attacks on AI systems, breach exposure linked to AI. |

workforce_impacts | AI-driven displacement, skills obsolescence, shadow AI usage by employees. |

regulatory_compliance | AI Act/GDPR/privacy obligations, IP/copyright risk, legal liability from AI decisions, regulatory uncertainty. |

information_integrity | AI-generated misinformation, deepfakes, content authenticity erosion, manipulation risk. |

reputational_ethical | Public trust erosion, algorithmic bias, ethical concerns, fairness, social licence risk. |

third_party_supply_chain | Vendor dependency/concentration risk, downstream misuse of third-party AI, over-reliance on AI providers. |

environmental_impact | Energy consumption and carbon footprint from AI training and inference. |

national_security | AI in critical infrastructure, geopolitical AI risks, security-of-state concerns, export controls. |

The initial risk taxonomy was developed from first principles and included the following categories: operational_technical, workforce_impacts, regulatory_compliance, information_integrity, reputational_ethical, third_party_supply_chain, environmental_impact, and national_security. However, during early classifier testing, we observed that cybersecurity and strategic_competitive risks were among the most frequently cited AI risk types in reports, yet did not fit well within the existing framework. As a result, these were introduced as additional categories.

We also ran an open-taxonomy test on a sample of 100 AI mentions to see whether the model would surface a cleaner alternative to the fixed risk categories. The result was not a more useful emergent taxonomy but a label-explosion problem: 96 successful runs produced 107 distinct labels, many of them near-duplicates or minor wording variants of the same underlying ideas. After manual consolidation, those labels collapsed back into a familiar set of broad themes such as regulatory/compliance, cyber/fraud, strategic competition, data governance, model ethics, reputational harm, workforce effects, and third-party dependence. This test taught us that the taxonomy we are using likely captures well the variety of AI risks mentioned in annual reports.

Stage 2c: Substantiveness

| Band | Definition |

|---|---|

boilerplate | Generic language with no information content; could appear unchanged in any company's report. |

moderate | Identifies a specific risk area, use case, or provider but lacks concrete mechanism, mitigation detail, deployment context, or quantification. |

substantive | Meets the disclosure-specific threshold for concrete, company-specific evidence. |

Note: the substantiveness definitions are operationally distinct. For risk, substantive requires a specific risk mechanism and concrete mitigation actions or commitments; for adoption, it requires named systems, quantified impact, or technical specificity; for vendor disclosure, it requires a named provider or model linked to a concrete use case, scale, or outcome. All three share the same bands for comparability.

Stage 2d: Vendor Tags

| Tag | Scope |

|---|---|

microsoft | Microsoft AI products: Azure AI, Copilot, Power Platform AI, Bing AI |

google | Google AI products: Gemini, Vertex AI, Google Cloud AI |

openai | OpenAI products: GPT series, ChatGPT, DALL·E |

amazon | Amazon/AWS AI services: Bedrock, SageMaker, Rekognition |

nvidia | Nvidia AI products: DGX, NIM microservices, Nvidia AI Enterprise |

meta | Meta AI products: Llama series, Meta AI |

salesforce | Salesforce AI products: Einstein AI, Agentforce |

ibm | IBM AI products: watsonx, Watson AI, IBM Cloud AI services |

databricks | Databricks: Mosaic AI, MLflow, Unity Catalog AI features |

snowflake | Snowflake AI: Cortex AI, Snowflake ML, Arctic |

anthropic | Anthropic products: Claude series |

xai | xAI products: Grok series |

palantir | Palantir AI platforms: AIP, Foundry, Gotham |

arm | Arm AI compute: Ethos NPUs, Arm Cortex AI infrastructure |

mistral | Mistral AI models: Mistral and Mixtral series |

uk_ai | UK-headquartered AI providers (e.g. Stability AI, BenevolentAI) |

open_source_model | Open-source models deployed without a named commercial provider |

internal | Company describes in-house or proprietary AI development |

other | Explicitly named provider not in the named-vendor list |

undisclosed | External AI capability referenced without naming the provider |

All classification was performed using Google's Gemini 3 Flash model with structured output. Prompt definitions for all classifiers are reproduced in full in Appendix A.

2.5 Validation

The pipeline was validated against a human-annotated sample set of 474 AI mentions drawn from 30 reports spanning two consecutive years (2023 and 2024) across 15 companies covering all 13 CNI sectors (see Appendix C). In addition, six models were evaluated before selecting Gemini Flash 3 as the production classifier, based on its accuracy, structured-output reliability, and cost. Notably, there was substantial divergence between the human-assigned labels and those generated by the LLM, with Jaccard similarity scores ranging from 0.75 to 0.23. Closer inspection revealed that the LLM consistently assigned more labels per report while maintaining perfect accuracy, capturing nuances that the human annotator had missed.

3. Limitations

3.1 Causal and Inferential Limits

The most fundamental limit is that often disclosure does not equal exposure. A company that discusses AI risk at length in its annual report is not necessarily more exposed to AI-related harm than a company that says nothing. It may simply have more sophisticated governance processes, be operating in a more heavily scrutinised sector, or be responding to investor or regulatory pressure. Conversely, a company with thin or absent AI disclosure may face significant operational AI risk that it has not yet recognised, has chosen not to disclose, or has disclosed under language our keyword gate does not capture. The corpus measures what companies say, not what they experience.

The 2023-2024 surge in AI risk mentions (an almost 200% increase in report count in a single year) is the most striking finding in the dataset and the most difficult to attribute. Three mechanisms are simultaneously operative and individually plausible: the mass-market adoption of generative AI tools (ChatGPT launched November 2022; enterprise GenAI adoption accelerated through 2023), early anticipatory compliance with the 2024 UK Corporate Governance Code as companies revised their risk frameworks ahead of Provision 293, and growing investor and analyst pressure to address AI risk specifically. We cannot cleanly decompose these effects with observational disclosure data alone.

3.2 Coverage Gaps

The corpus covers 1,362 companies that together account for around 20% of the UK's GDP. However, it does not provide insight into all 5.7 million private sector businesses operating in the UK, so it should be treated only as a proxy for the wider economy.

178 companies have zero coverage from FinancialReports.eu despite appearing in that source's filing index, in some cases because the source misclassifies non-annual-report documents (for example, Jet2 PLC's prospectus and share-buyback notices were returned as annual-report candidates). The Companies House gap-fill reduces but does not fully resolve this exposure, and any systematic pattern in which companies are missed could introduce a modest sector-level bias.

The UK-only scope of the corpus is a limitation for generalisability. The regulatory architecture underpinning UK annual reports differs from the SEC mandatory-disclosure regime for US 10-Ks, ESEF for European-listed companies, and the very different reporting cultures of other major jurisdictions. Findings about disclosure patterns, sector composition, and quality should not be assumed to transfer directly to other markets. The pipeline methodology, however, is jurisdiction-neutral and can be applied to any structured machine-readable filing corpus.

Finally, annual reports are a lagging instrument. They reflect decisions, risks, and governance arrangements as they existed at the close of a fiscal year, typically published three to four months later and sometimes consulted many months after that. The Observatory captures where companies were, not where they are.

3.3 Classification Validity

The primary validation instrument is a human-annotated golden set of 474 chunks reviewed against the full two-stage classifier pipeline. This is a larger evaluation corpus than many comparable studies in financial-NLP research, but it remains a constraint on our ability to estimate sub-category precision independently. In particular, rare signal types (such as: agentic adoption, national security risk, and sector-specific vendor mentions) appear infrequently enough in the golden set that sub-category confidence intervals remain wide.

The pipeline's conservative prompting strategy is a deliberate design choice: it reduces false positives, but at the cost of potentially missing some genuine AI mentions. By requiring explicit AI language at Stage 1 and refusing to infer adoption from intent or strategy statements alone, the classifier excludes some passages that a human annotator might reasonably flag. Companies that describe AI capabilities obliquely, through references to "intelligent systems," "predictive tools," or proprietary platform features without explicit AI attribution, will not be captured. The pipeline therefore produces a conservative lower bound on AI disclosure activity rather than an upper bound.

Substantiveness classification is where judgement-dependent is more “subtle” than mention-type and risk-category classifiers. The substantiveness scale (boilerplate / moderate / substantive) requires the classifier to make fine-grained judgements between similar passages, assessing specificity, level of concrete detail, and whether actual governance actions or controls are described; for this reason, substantiveness scores are approximate indicators of disclosure quality and broad reporting patterns, not exact measurements.

Vendor tagging carries its own opacity. The "other" category captured 154 signals in 2025 alone, and "undisclosed" represents an additional 65 references where vendor identity cannot be inferred from the disclosure text. Until reporting practice improves, vendor concentration analysis at the firm level will remain limited by the deliberate or inadvertent opacity of the source documents themselves.

4. Findings

All figures cover publication years 2020 to 2025 unless otherwise stated. 2026 data is partial (only 339 reports) and is not used for trend conclusions unless stated otherwise. Report-level counts reflect unique company-year filings containing at least one signal of the relevant type; a single report may contribute to multiple signal categories. Risk-category and adoption-type counts are label assignments and may exceed unique report counts.

4.1 The Disclosure Surge: Overall Trends

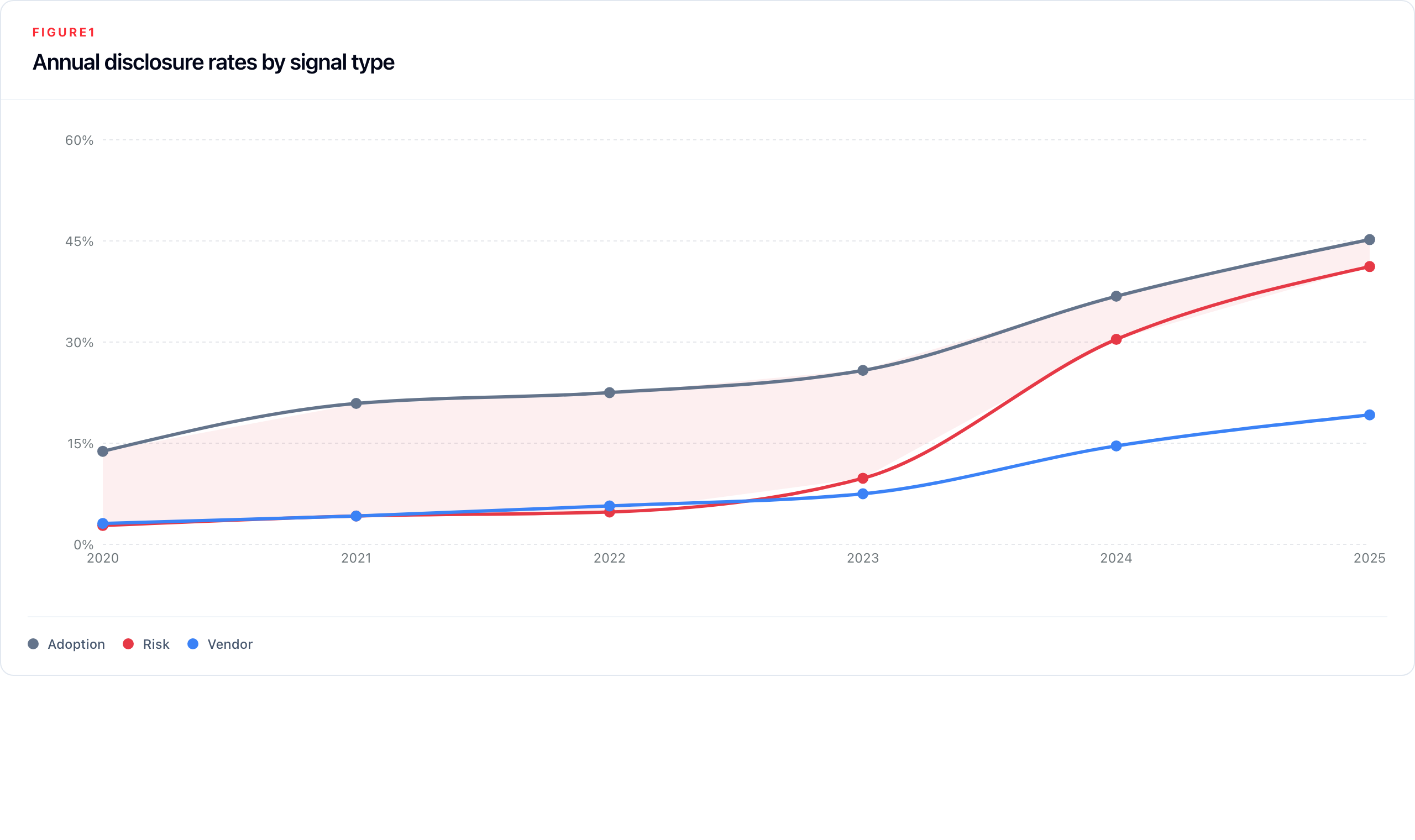

The most striking finding in the corpus is the scale and speed of growth in AI-related disclosure. In 2020, 199 of 1,007 processed reports (19.8%) contained at least one AI mention. By 2025, that figure had risen to 1,023 of 1,561 reports, or 65.5%. Risk disclosure grew even faster from a much smaller base: in 2020, just 28 reports (2.8%) named AI as a material risk. By 2025, 643 reports (41.2% of the annual cohort), a 23-fold increase in absolute terms. Table 2 provides the full year-by-year breakdown.

Table 2: Annual disclosure prevalence by signal type (% of all reports that year)

| Year | Reports | Any AI | Adoption | Risk | Vendor | Adoption-Risk gap |

|---|---|---|---|---|---|---|

| 2020 | 1,007 | 19.8% | 13.8% | 2.8% | 3.1% | 11.0 pp |

| 2021 | 1,328 | 27.4% | 20.9% | 4.2% | 4.2% | 16.6 pp |

| 2022 | 1,853 | 28.4% | 22.5% | 4.8% | 5.7% | 17.6 pp |

| 2023 | 1,905 | 36.8% | 25.8% | 9.8% | 7.5% | 16.1 pp |

| 2024 | 1,828 | 55.2% | 36.8% | 30.4% | 14.6% | 6.4 pp |

| 2025 | 1,561 | 65.5% | 45.2% | 41.2% | 19.2% | 4.0 pp |

The Adoption-Risk gap in the table above shows the percentage of reports that mention adoption for that year minus the percentage that mention AI risk. The spread between these two variables is highlighted in Figure 1 below.

Growth across the full period falls into three broadly distinct phases. Between 2020 and 2022, adoption disclosure grew steadily, from 13.8% to 22.5% of reports, while risk disclosure lagged, reaching only 4.8% by 2022. The adoption-to-risk gap widened over this phase, peaking at 17.6 percentage points in 2022, as companies began describing their AI use without yet framing it as a governance concern. The second phase opens in 2023: risk mentions more than doubled in a single year (4.8% → 9.8%), as ChatGPT reached mass awareness and AI moved rapidly from a technology consideration to a board-level agenda item. The third phase, 2024 onwards, is defined by the risk disclosure surge: risk reports almost tripled in a single year (9.8% → 30.4%), compressing the adoption-risk gap from 16.1 to 6.4 percentage points. By 2025, the gap had narrowed to 4.0 pp; risk disclosure is now close to parity with adoption disclosure. In the partial 2026 data, risk reports (66.4%) exceed adoption reports (63.1%) for the first time, suggesting the two signals may have crossed.

Despite this growth, the disclosure gap remains substantial in absolute terms. In 2025, 918 of 1,561 annual reports (58.8%) contained no AI risk mention.

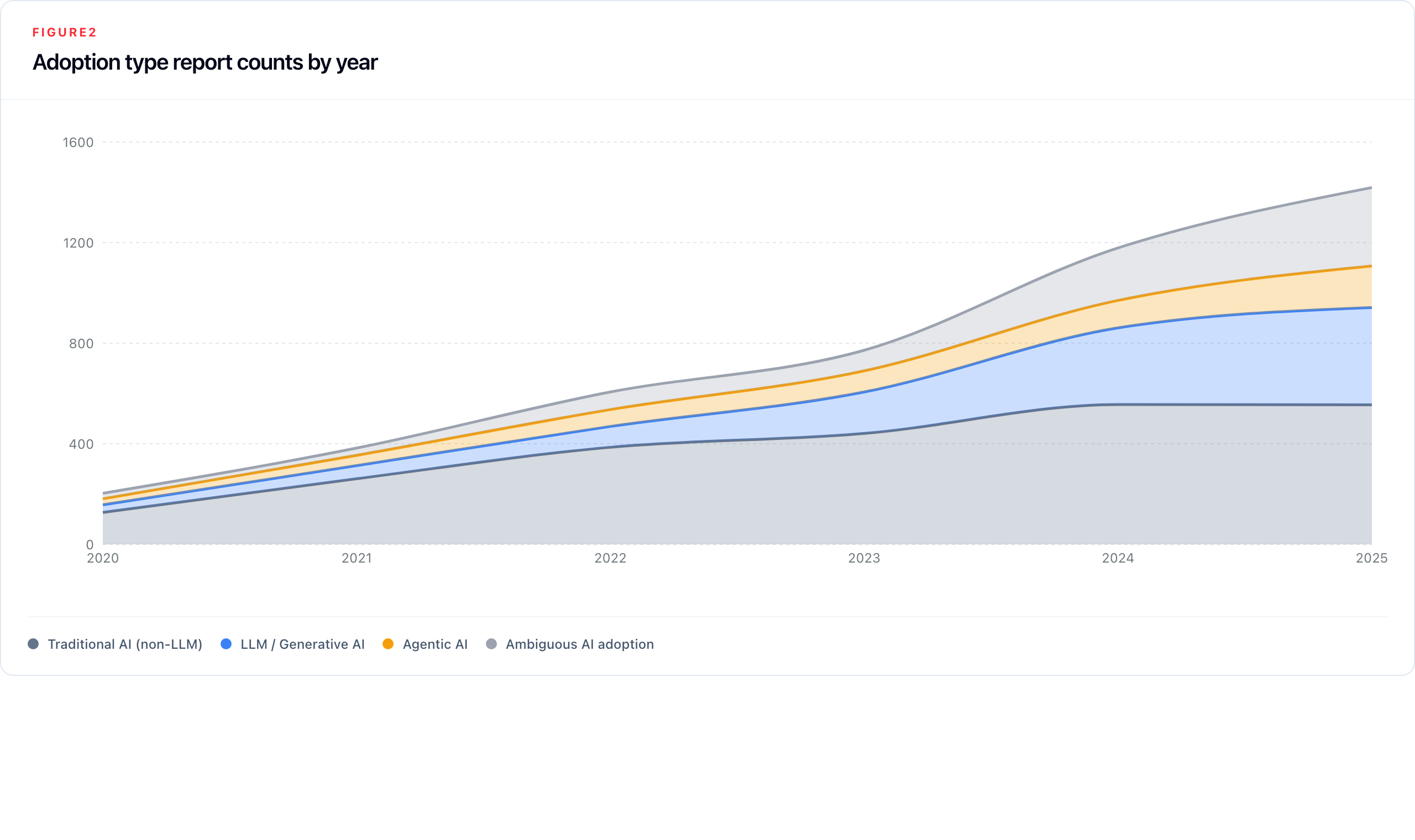

4.2 Adoption Patterns

Adoption disclosure appeared in 2,916 unique company-year filings across the full corpus. Its composition has shifted significantly over time as the balance between AI types has reordered.

Table 3: Adoption type disclosure rates (% of all reports), 2024–2025

| Adoption type | 2024 | 2025 | YoY change |

|---|---|---|---|

| Traditional AI (non-LLM) | 30.4% | 35.6% | +5.1 pp |

| LLM / Generative AI | 16.7% | 24.8% | +8.1 pp |

| Agentic AI | 6.0% | 10.6% | +4.6 pp |

| Ambiguous AI adoption | 11.4% | 20.0% | +8.6 pp |

Non-LLM adoption (traditional machine learning, computer vision, predictive analytics, fraud detection) remains the numerically dominant category, growing from 127 reports in 2020 to 555 in 2025. But LLM and generative AI adoption has grown faster (13-fold versus four-fold for non-LLM) - and by 2025 LLM adoption appears in 24.8% of all reports, narrowing on non-LLM at 35.6%. LLM adoption was essentially invisible before 2022; its acceleration is the clearest signal in the corpus of the ChatGPT diffusion effect translating into formal corporate disclosure.

Agentic AI (autonomous systems that execute tasks without continuous human oversight) appears in 165 reports by 2025, up from 24 in 2020. The category is growing in significance beyond its absolute count: average adoption labels per adoption-reporting company rose from 1.75 in 2024 to 2.01 in 2025, partly driven by companies reporting multiple adoption types simultaneously as AI deployment portfolios diversify. Agentic AI mentions are concentrated in Finance, Transport, and Defence.

The ambiguous adoption category reached 312 label assignments in 2025, or 20.0% of all reports. It represents companies acknowledging AI adoption without enough operational specificity to classify the use as non-LLM, LLM/generative, or agentic. Its growth reflects a reporting environment where mentioning AI has become normative but concrete characterisation has not.

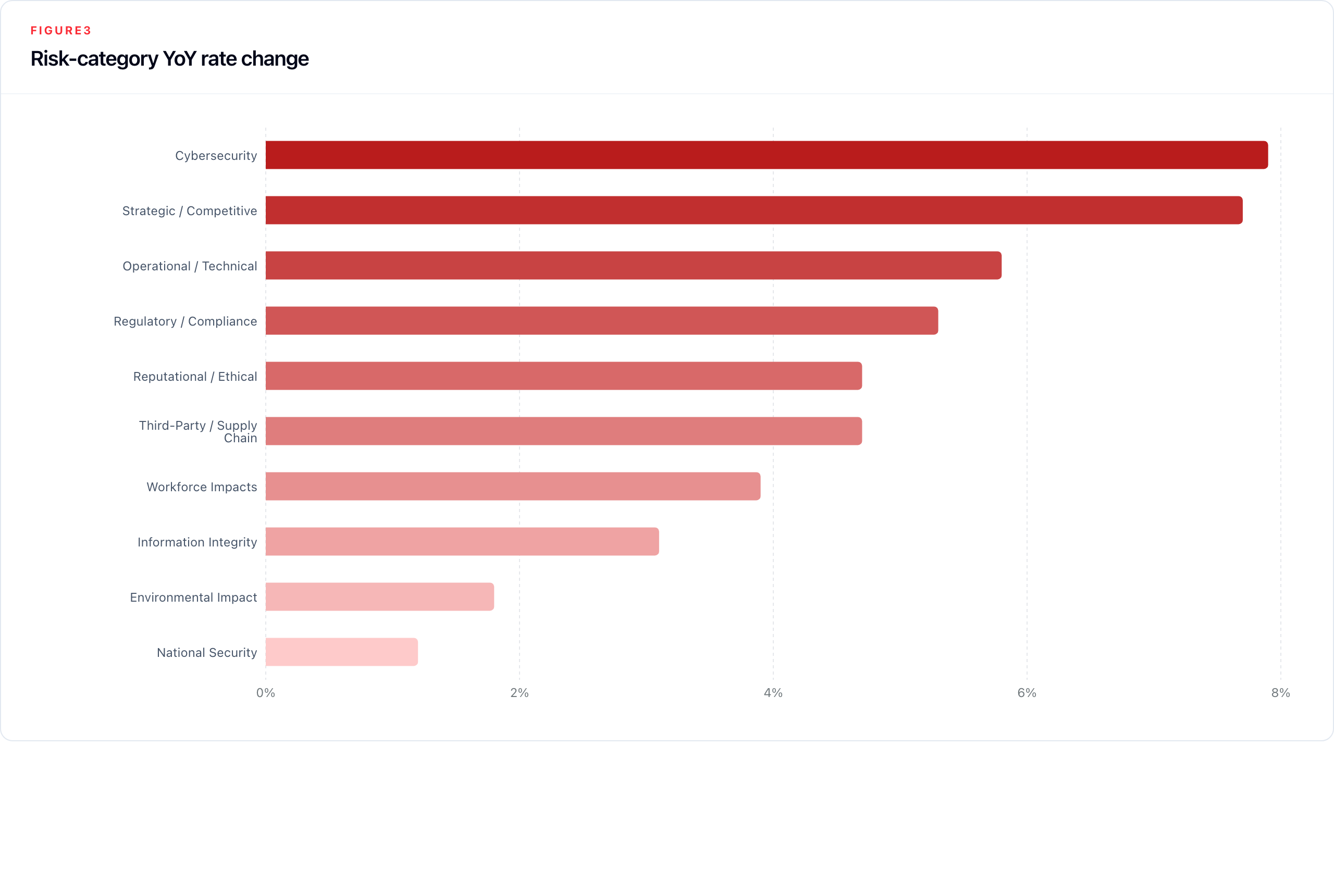

4.3 Risk Disclosure Patterns

AI risk mentions not only grew in volume but broadened substantially in scope. In 2020, the risk profile was narrow: strategic/competitive and operational/technical together were the most prominent AI risk tags. By 2025, all ten taxonomy categories are materially represented, the risk profile has diversified, and companies reporting risk are reporting more of it: average risk labels per risk-reporting company rose from 3.42 in 2024 to 3.65 in 2025.

Table 4: Risk category disclosure rates (label assignments as % of all 2025 reports), 2024–2025

| Risk category | 2025 assignments | 2025 % of reports | 2024 % of reports | YoY change |

|---|---|---|---|---|

| Cybersecurity | 401 | 25.7% | 17.8% | +7.9 pp |

| Strategic / Competitive | 427 | 27.4% | 19.6% | +7.7 pp |

| Operational / Technical | 377 | 24.2% | 18.3% | +5.8 pp |

| Regulatory / Compliance | 320 | 20.5% | 15.2% | +5.3 pp |

| Reputational / Ethical | 248 | 15.9% | 11.2% | +4.7 pp |

| Third-Party / Supply Chain | 191 | 12.2% | 7.5% | +4.7 pp |

| Workforce Impacts | 132 | 8.5% | 4.5% | +3.9 pp |

| Information Integrity | 162 | 10.4% | 7.3% | +3.1 pp |

| Environmental Impact | 45 | 2.9% | 1.1% | +1.8 pp |

| National Security | 42 | 2.7% | 1.5% | +1.2 pp |

Strategic/competitive risk remains the largest category by assignment count (27.4%), but the fastest compositional shift is the rise of cybersecurity: from 9 reports in 2020 to 401 in 2025, it has moved from a peripheral concern to the second-largest category and was the fastest-rising risk label in 2025. This represents a reframing of AI in corporate risk language, from a strategic threat (competitive obsolescence) to an operational one (AI-enabled attacks, adversarial exploitation, AI-accelerated fraud), consistent with NCSC guidance on AI as a force multiplier for hostile actors.

Two categories show exceptional growth from near-zero bases. Information integrity (AI-generated misinformation, deepfakes, content authenticity erosion) grew from 1 report in 2020 to 162 in 2025. Workforce impacts grew from 3 to 132 reports, a 44-fold increase. Their emergence as mainstream disclosure categories reflects how the perceived scope of AI risk has broadened from competitive and technical concerns to societal and human-capital questions. National security2, while small (42 reports in 2025), is non-trivially concentrated in CNI sectors and growing in the 2026 partial data.

Critically, the directness of risk attribution improved only modestly. The distribution of signal strength (the classifier's rating of how explicitly AI is attributed as the risk source) shifted from 30.6% explicit (signal 3) in 2024 to 33.2% in 2025; strong implicit (signal 2) moved from 29.8% to 28.8%; weak implicit (signal 1) fell from 39.6% to 38.0%. Companies are disclosing more risk categories, but direct attribution to AI is improving much more slowly than disclosure volume.

4.4 Harm Classifications

The pipeline includes a harm label for AI described as having caused a past, specific incident (misinformation spread, fraud enabled by AI, a safety failure, or a discriminatory outcome), as distinct from prospective risk. Across the full 9,821-report corpus, harm classifications are almost entirely absent: nine harm-tagged chunks were identified across seven company-year filings. The affected filings are Polar Capital Technology Trust PLC in 2020 and 2024, Prudential PLC in 2022, AstraZeneca PLC in 2024 and 2025, Gear4Music (Holdings) PLC in 2025, and Trifast PLC in 2025. Four of the five companies are CNI-sector operators (Finance or Health); Gear4Music is the sole non-CNI company.

This near-absence is most likely a genuine feature of the annual report as a disclosure format. Companies have strong legal and reputational incentives to avoid admitting past AI-related harms in a board-accountable document, and will typically frame incidents as risks managed or lessons learned rather than harms caused. The annual report is therefore not a reliable surface for detecting realised AI incidents, and other data sources (regulatory enforcement records, incident databases, litigation filings) would be needed to complement the Observatory's signals on this dimension.

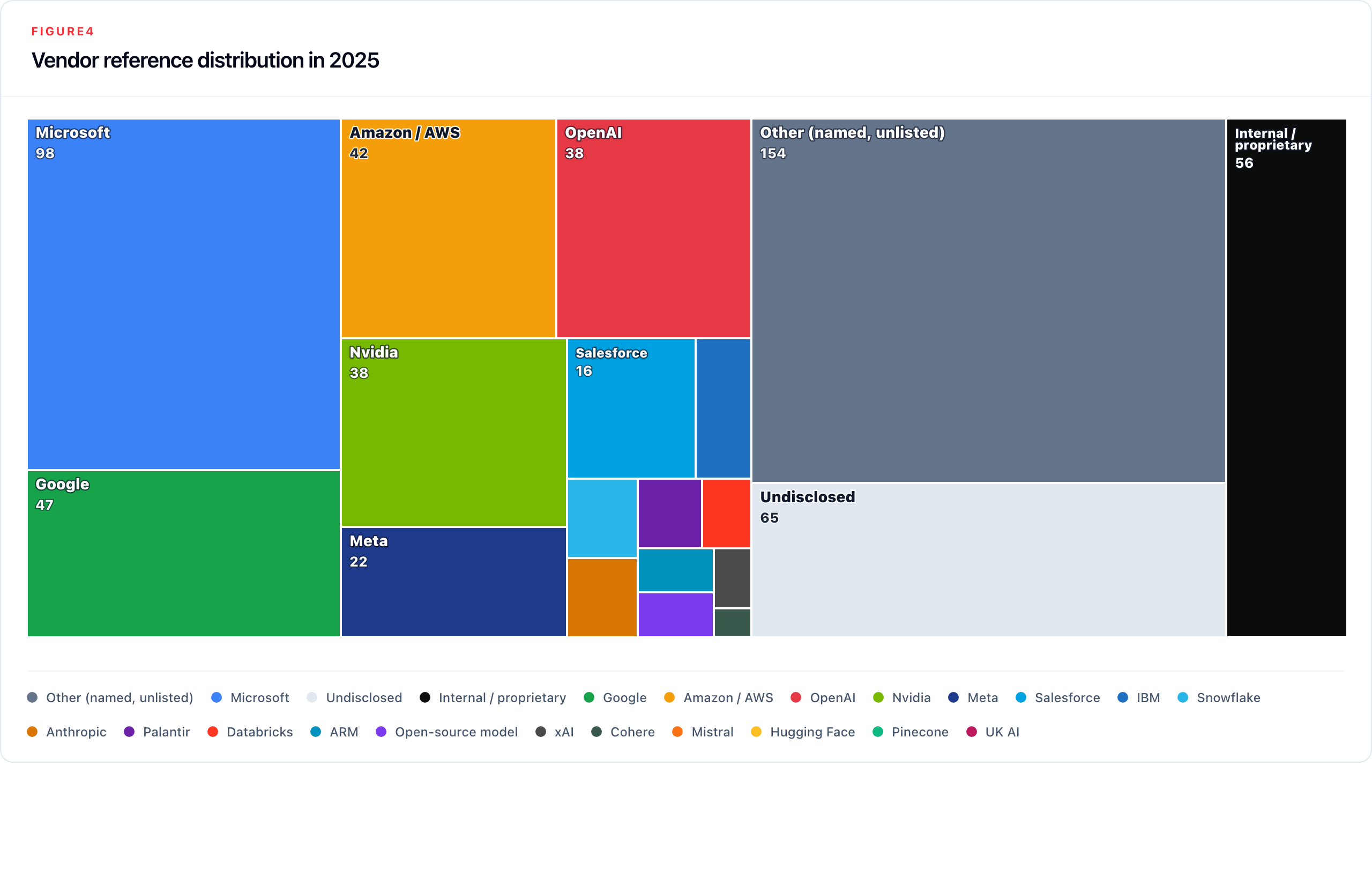

4.5 The Vendor Landscape

Vendor references appeared in 1,001 unique company-year filings. The distribution is heavily skewed, and its most important feature is not which vendors are named but how many are not.

Table 5: Vendor reference rates (label assignments as % of all 2025 reports), 2024–2025

| Vendor | 2025 assignments | 2025 % of reports | 2024 % of reports | YoY change |

|---|---|---|---|---|

| Other (named, unlisted) | 154 | 9.9% | 5.9% | +4.0 pp |

| Microsoft | 98 | 6.3% | 6.1% | +0.2 pp |

| Undisclosed | 65 | 4.2% | 1.8% | +2.4 pp |

| Internal / proprietary | 56 | 3.6% | 2.5% | +1.1 pp |

| 47 | 3.0% | 2.7% | +0.3 pp | |

| Amazon / AWS | 42 | 2.7% | 2.1% | +0.6 pp |

| OpenAI | 38 | 2.4% | 3.8% | −1.3 pp |

| Nvidia | 38 | 2.4% | 3.1% | −0.6 pp |

| Meta | 22 | 1.4% | 1.0% | +0.4 pp |

| Salesforce | 16 | 1.0% | 0.5% | +0.5 pp |

| IBM | 7 | 0.4% | 0.4% | +0.1 pp |

| Anthropic | 5 | 0.3% | 0.1% | +0.2 pp |

| Snowflake | 5 | 0.3% | 0.1% | +0.2 pp |

| Databricks | 3 | 0.2% | 0.2% | 0.0 pp |

| ARM | 3 | 0.2% | 0.3% | −0.1 pp |

| Open-source model | 3 | 0.2% | 0.1% | +0.1 pp |

| Palantir | 4 | 0.3% | 0.0% | +0.3 pp |

| xAI | 2 | 0.1% | 0.0% | +0.1 pp |

| Cohere | 1 | 0.1% | 0.0% | +0.1 pp |

Two findings stand out. First, other and undisclosed together (references to external AI capabilities without identifying the provider) account for 219 of 609 total 2025 vendor assignments, or 36.0% of all vendor references. Among only explicitly named vendors, the three largest account for 56.0% of named-vendor assignments, still revealing substantial concentration. Second, OpenAI is the largest declining named vendor year-on-year (−1.3 pp), which may reflect a combination of reduced direct API usage and the routing of OpenAI model access through Azure, which registers as Microsoft; Nvidia also declined (−0.6 pp). This structural opacity means that concentration at the foundation-model layer may be larger than the named-vendor data alone suggests.

Vendor disclosures are comparatively concrete when the provider is named. The remaining policy problem is incomplete dependency mapping: companies are acquiring AI capabilities from a small number of providers but not consistently identifying those dependencies as material disclosure items.

4.6 Disclosure Quality: The Substantiveness Gap

Substantiveness scoring covers the three main Phase 2 outputs. The 2025 distribution shows a clear hierarchy: vendor disclosures are usually concrete, adoption disclosures are mostly moderate, and risk disclosures remain overwhelmingly moderate.

Table 6: 2025 disclosure substantiveness by classifier

| Disclosure type | Scored reports | Substantive | Moderate | Boilerplate |

|---|---|---|---|---|

| Adoption | 705 | 238 (33.8%) | 391 (55.5%) | 76 (10.8%) |

| Risk | 643 | 67 (10.4%) | 505 (78.5%) | 71 (11.0%) |

| Vendor | 299 | 193 (64.5%) | 74 (24.7%) | 32 (10.7%) |

Pure boilerplate is not the dominant disclosure mode in 2025. The larger problem is moderate disclosure: companies name an AI use, risk, or provider, but usually do not explain the mechanism, operational context, mitigation, scale, or outcome.

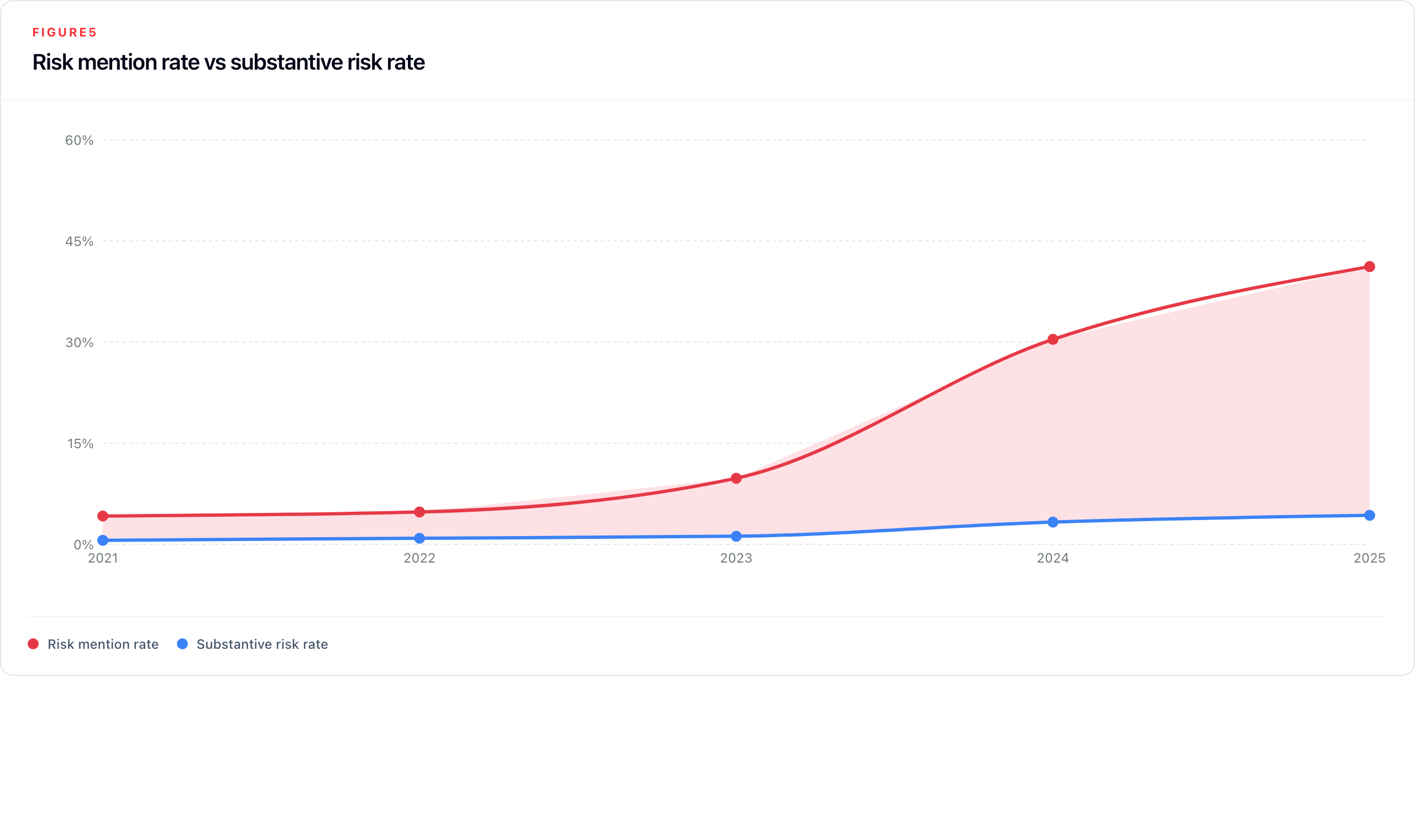

Risk remains the central policy concern because it is the disclosure type most directly tied to board-level controls. Table 7 shows risk mention rates rising far faster than substantive risk rates through the core 2021–2025 window.

Table 7: Quality-gap analysis: risk mention rate vs substantive risk rate

| Year | Risk reports | Risk rate | Substantive risk reports | Substantive risk rate | Quality gap |

|---|---|---|---|---|---|

| 2021 | 56 | 4.2% | 8 | 0.6% | 3.6 pp |

| 2022 | 89 | 4.8% | 16 | 0.9% | 3.9 pp |

| 2023 | 186 | 9.8% | 23 | 1.2% | 8.6 pp |

| 2024 | 556 | 30.4% | 61 | 3.3% | 27.1 pp |

| 2025 | 643 | 41.2% | 67 | 4.3% | 36.9 pp |

Signal strength data corroborates this independently: the share of explicit risk signals (signal 3) was 30.6% in 2024 and 33.2% in 2025, while weak-implicit signals fell from 39.6% to 38.0%. Companies are acknowledging more risk categories much faster than they are improving direct attribution to AI.

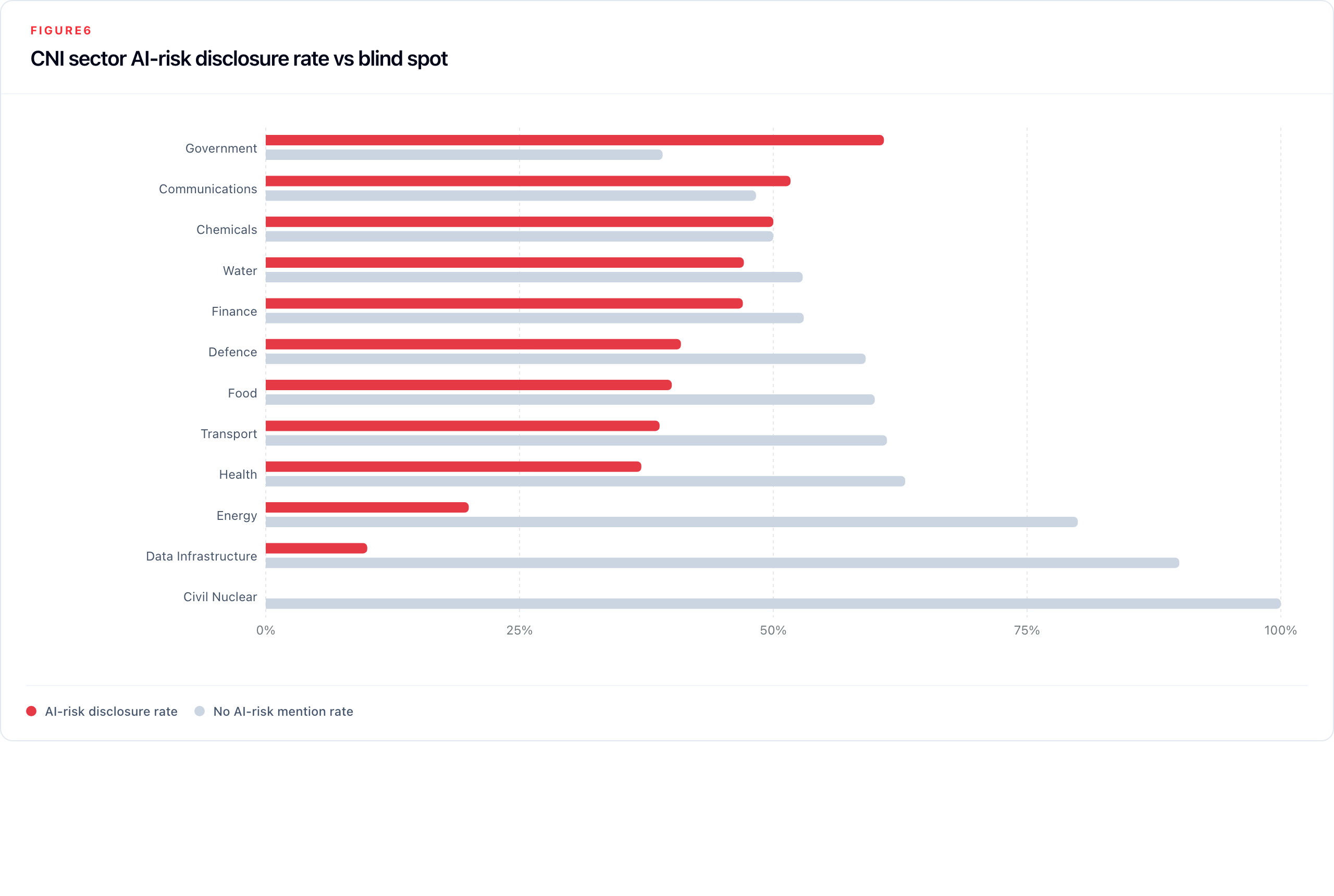

4.7 Sector and CNI Patterns

Sector-level findings reveal sharp variation in both disclosure intensity and disclosure depth across the UK's Critical National Infrastructure framework. Table 8 provides the full 2025 breakdown.

Table 8: CNI sector disclosure summary (2025)

| Sector | Companies | 2025 reports | AI mention % | AI risk % | Risk YoY change |

|---|---|---|---|---|---|

| Government | 20 | 23 | 87.0% | 60.9% | +2.5 pp |

| Communications | 28 | 29 | 86.2% | 51.7% | +26.7 pp |

| Chemicals | 34 | 24 | 62.5% | 50.0% | +21.1 pp |

| Water | 18 | 17 | 64.7% | 47.1% | +13.7 pp |

| Finance | 461 | 657 | 74.7% | 47.0% | +10.7 pp |

| Defence | 20 | 22 | 77.3% | 40.9% | +14.0 pp |

| Food | 52 | 70 | 62.9% | 40.0% | +8.4 pp |

| Transport | 61 | 67 | 73.1% | 38.8% | +12.3 pp |

| Health | 111 | 100 | 50.0% | 37.0% | +7.3 pp |

| Energy | 141 | 140 | 30.7% | 20.0% | +5.9 pp |

| Data Infrastructure | 22 | 20 | 60.0% | 10.0% | +5.0 pp |

| Civil Nuclear | 2 | 3 | 0.0% | 0.0% | n/a |

Finance dominates in absolute volume (461 companies, all ten risk categories materially represented), and its disclosure depth reflects genuine AI embeddedness across trading, credit, fraud detection, and compliance. Communications had the largest single-year rise in risk disclosure in 2025 (+26.7 pp), consistent with the sector's exposure to both AI-enabled content moderation and information integrity risks. Government leads on AI mention rate (87.0%) and risk rate (60.9%), with workforce impacts its most prominent risk category, consistent with the public policy debate around AI in public services.

Two sectors warrant particular attention. Data Infrastructure talks about AI risk the least: 90.0% of reports in 2025 contain no AI risk mention, despite this sector's role as the layer on which most AI deployment depends. Energy is close behind at 80.0%, even though AI is increasingly embedded in grid management, predictive maintenance, and operational technology, and OT/IT convergence in energy infrastructure is among the most documented systemic risk concerns in the national security literature. These low disclosure rates should not be read as evidence of low exposure; they identify sectors where public annual-report disclosure appears thin relative to plausible AI relevance.

Water reached 47.1% AI risk disclosure in 2025 (up from 33.3% in 2024), a rise that partly reflects the small sample size (17 reports from 18 companies) amplifying individual company changes. The absolute numbers warrant caution, but the direction is notable.

Defence reports a high adoption of agentic AI. It is the only sector with agentic tags (31) outnumbering LLM signals (15). This is consistent with defence sector language around autonomous systems, vehicles, and unmanned platforms.

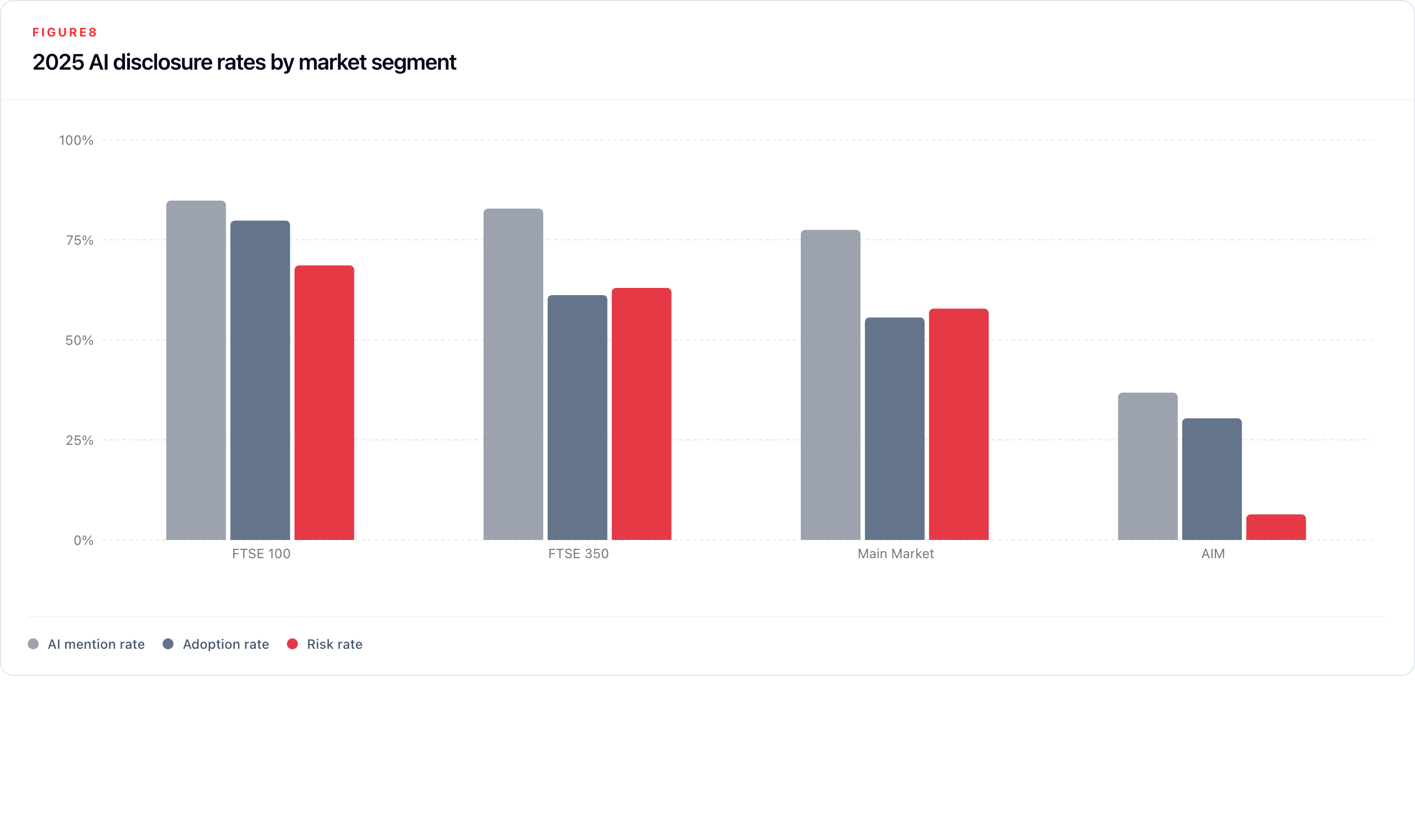

4.8 Market Segment Patterns

The gap between Main Market and AIM disclosure is one of the most structurally significant findings in the corpus. Table 9 presents 2025-specific rates, which are materially higher than lifetime rates and provide the clearest picture of the current state.

Table 9: Market segment disclosure summary (2025)

| Market segment | Lifetime reports | 2025 reports | 2025 AI mention % | 2025 Adoption % | 2025 Risk % | 2025 Vendor % |

|---|---|---|---|---|---|---|

| FTSE 100 | 1,359 | 223 | 84.8% | 79.8% | 68.6% | 31.8% |

| FTSE 350 | 3,638 | 606 | 82.8% | 61.2% | 63.0% | 28.9% |

| Main Market | 4,166 | 703 | 77.5% | 55.6% | 57.8% | 25.6% |

| AIM | 1,414 | 171 | 36.8% | 30.4% | 6.4% | 9.4% |

In 2025, 68.6% of FTSE 100 companies mentioned AI risk in their reports. The question for the largest companies is no longer whether they disclose AI risk but whether these mentions have valuable information or are boilerplate in nature.

AIM is in a different category. Only 6.4% of companies in 2025 mentioned AI as a risk, against 57.8% for the Main Market. The gap in AI risk mentions is wider than the gap in general mentions of AI (36.8% AI mention for AIM, suggesting companies are aware of AI; 6.4% risk, suggesting they may not translate that awareness into formal risk governance).

5. Related Work

This Observatory draws on four research directions: financial disclosure Natural Language Processing (NLP), the study of substantiveness and boilerplate in regulated reporting, empirical work on AI disclosure and governance, and observatory-style monitoring systems applied to other risk domains. Together these streams guide some of the design choices described in Section 2.

5.1 Financial Disclosure NLP

The application of natural language processing to corporate filings has a well-developed lineage, anchored by the observation that financial language is domain-specific enough to require special approaches. Loughran and McDonald (2011) provided the foundational demonstration of this problem: showing that generic sentiment dictionaries, built on general English corpora, systematically misclassify financial text. Their construction of a finance-specific word list, and their evidence linking filing language to market outcomes, established annual reports as a legitimate and productive NLP corpus. Their subsequent survey of the field (Loughran & McDonald, 2016) maps the methodological terrain (tone, readability, topic extraction, risk language, and document length) and provides the framework within which subsequent work, including this Observatory, situates its design choices.

The question of whether textual analysis methods developed on US 10-K filings generalise to other jurisdictions is addressed directly by Lang and Stice-Lawrence (2015), whose study of international annual reports demonstrates that large-sample NLP analysis of non-US filings is both feasible and informative, while noting that disclosure norms, regulatory environments, and reporting cultures vary across markets. This finding supports the treatment of UK annual reports as a valid corpus for structured analysis while reinforcing the need for UK-specific calibration of any taxonomy or classifier.

More recent work has extended this tradition to large language models. Kim (2024) demonstrates that LLMs can extract decision-relevant signals from financial statements at scale, producing outputs that are competitive with or superior to specialised financial models on several evaluation tasks. Park and colleagues (BIS/IFC, 2024) apply LLM-based agents specifically to the problem of materiality assessment in risk disclosures, identifying which disclosed risks are substantive enough to affect investment decisions, a task closely analogous to the substantiveness classification in our pipeline.

5.2 Substantiveness and Boilerplate

A closely related literature examines the tendency for mandatory reports to accumulate length and repetition without commensurate growth in informational content. Dyer, Lang and Stice-Lawrence (2017) document this across US 10-K filings, showing that reports have grown substantially longer while becoming more redundant and less specific, a pattern they attribute to regulatory accretion, legal caution, and the incentive to copy prior-year language rather than update it. This evidence of systematic disclosure inflation provides the empirical motivation for the Observatory's substantiveness classifier.

Brown and Tucker (2011) provide the most comprehensive empirical work on the disclosure quality of this type, showing that year-over-year textual modification in the Management's Discussion and Analysis (MD&A) section of 10-Ks serves as a proxy for informational updating: reports that change more tend to carry more new information. The economics of boilerplate are not merely aesthetic. Generic risk factor language has historically provided legal protection under safe-harbour provisions, creating a rational incentive for companies to disclose broadly without disclosing specifically. Regulatory pressure on both sides of the Atlantic has begun to push against this: the SEC's 2024 State of Disclosure Review extended this pressure specifically to AI, noting that AI disclosure had grown rapidly but remained in many cases untailored and insufficiently tied to actual business use.

5.3 AI Disclosure and Governance

Empirical research on AI disclosure in corporate filings has accelerated markedly since 2022, though it remains concentrated on US SEC filings. Uberti-Bona Marin and colleagues (2025) provide the most directly comparable large-scale study: analysing more than 30,000 filings from over 7,000 US firms, they document a steep rise in AI risk mentions between 2020 and 2024, with over 50% of firms mentioning AI in their annual filings by 2024, a pattern consistent in direction with the UK findings reported here. Critically, they also find that many disclosures remain generic and thin on mitigation detail, mirroring the substantiveness gap we document for UK risk disclosure.

In the UK specifically, a 2025 study of AI narratives in FTSE 100 annual reports (2020–2023) frames AI disclosure as a form of strategic communication and impression management rather than straightforward risk reporting. Companies shape their AI narratives to signal ambition to investors, not only to discharge disclosure obligations. This framing supports our design choice to maintain a separate General or Ambiguous label for AI mentions that are real but not classifiable into information-carrying content.

Bonsón and colleagues (2023) examine algorithmic decision-making disclosures in major Western European companies, finding that practice is uneven and largely voluntary. Chiu (2025) raises a related but distinct concern: as companies begin using generative AI in the drafting of narrative disclosures themselves, the authorship and reliability of the text being analysed changes in ways that are difficult to detect.

5.4 Observatory-Style Monitoring Systems

The closest methodological precedents for this Observatory come from climate and ESG monitoring, where researchers already use thematic taxonomies, domain-specific classifiers, and structured corporate corpora to track disclosure change over time. ClimateBERT (Webersinke et al., 2023) shows that specialist models can classify climate-risk disclosure at scale and expose the gap between disclosure volume and decision-useful specificity. Ferjančič et al. (2024) provide the closest UK analogue, using BERTopic on a decade of FTSE 350 annual reports to show that ESG themes shift measurably with regulation and major events. Supervisory work by the Bank of England, FCA, and BIS/IFC further confirms that large report corpora can be systematically read for policy-relevant risk signals.

The AI Risk Observatory applies that established monitoring logic to AI risk and adoption in UK annual reports. Its contribution is the domain and measurement design: UK annual reports rather than US 10-Ks, explicit CNI sector decomposition, vendor-dependency signals, and a substantiveness dimension that distinguishes mention frequency from disclosure quality.

6. Discussion and Implications

6.1 Applications and Use Cases

Regulatory benchmarking. The Provision 29 obligation, which requires boards to declare the effectiveness of all material internal controls, enters its first full annual reporting cycle for fiscal years beginning on or after 1 January 2026. The Observatory provides a pre-intervention baseline across the full universe of UK listed companies at a granularity (company, sector, market segment, and disclosure type) that enables clean before-and-after comparison. Rerunning the pipeline on FY2026 reports will produce a direct measure of whether the Code amendment delivers substantiveness improvement or merely increases disclosure volume.

Supervisory prioritisation. Regulators and sector bodies can use the corpus to identify companies with high plausible AI exposure and low disclosure, as a screening tool for follow-up supervisory inquiry. A company in the Water or Communications CNI sector with zero AI signal across multiple years is not necessarily unexposed; it may be a candidate for direct supervisory engagement. The Observatory does not replace supervisory judgment, but it provides a structured starting point that narrows the search space.

Research replication and jurisdictional comparison. The pipeline is fully documented, the classifier taxonomy is explicit, and the prompts are versioned. Any jurisdiction with access to machine-readable annual report filings (ESEF in the EU, 10-K EDGAR filings in the US, or equivalent national repositories) can run the same pipeline against its own corpus and produce directly comparable signals.

Annual report as a hard disclosure baseline. Earnings calls, investor presentations, and corporate surveys are softer forms of AI disclosure: they are not audited, not legally mandated to discuss principal risks, and produced for audiences with very different information needs. Annual reports occupy a distinct position in the information ecosystem as a legally accountable, audited, structured statement of what a company presents as its material risks and capabilities. The Observatory's signals can serve as a hard disclosure baseline against which softer disclosure channels are compared.

6.2 Future Work

Provision 29 follow-through is the highest-priority empirical next step. The 2024 surge in risk mentions may represent genuine governance improvement that will be consolidated in the first post-Provision-29 reporting cycle, or it may represent anticipatory disclosure volume not matched by underlying governance depth. Only the 2026 and 2027 report cohorts will resolve this.

Substantiveness integration by sector, segment, and company is the next methodological step. Adoption, risk, and vendor substantiveness are now scored at annotation level; the remaining work is to roll those fields into stable dashboard artefacts for sector, market-segment, company-transition, and year-over-year persistence analysis.

Causal modelling would connect disclosure signals to external data sources (cyber incident databases, AI-related regulatory enforcement actions, sector-level employment data, or company-level stock volatility around AI announcements) to test whether annual-report language predicts, follows, or is orthogonal to real-world AI-related outcomes.

Boilerplate tracking over time within companies is a direct extension of Brown and Tucker's (2011) MD&A modification measure applied to AI-specific language. By computing year-over-year textual similarity of AI-risk passages within the same company, it becomes possible to operationalise "disclosure staleness" at the firm level, identifying companies that have copied forward risk language for multiple years without material revision.

Agentic and autonomous system monitoring warrants dedicated attention. The agentic adoption category recorded approximately seven-fold growth between 2020 and 2025 (24 to 165 signals), a pace considerably faster than non-LLM adoption. Annual reports are beginning to describe autonomous AI agents in operational contexts: systems that act, not merely systems that analyse. The risk taxonomy, the disclosure patterns, and the governance language around agentic systems are likely to differ substantially from what has developed around predictive analytics and language models. Establishing a monitoring baseline for this category before it matures into a common disclosure topic will be considerably easier than retrospectively reconstructing it.

7. Conclusion

The AI Risk Observatory documents a disclosure landscape defined by volume growth without equivalent quality growth. AI disclosure is now a mainstream feature of UK annual reports, and risk disclosure has grown even faster. Across the broader quality picture, vendor disclosures are the most concrete, adoption disclosures are mostly moderate, and risk disclosures remain the weakest.

The sector and market segment findings reinforce this picture. Finance and Health are active disclosers; Data Infrastructure and Energy disclose less, despite plausible AI relevance. FTSE 100 companies are approaching saturation for general AI mentions, though risk disclosure and substantiveness still leave room for improvement. AIM companies remain structurally underrepresented in AI-risk disclosure, reflecting lighter governance obligations and reporting capacity as well as possible differences in company size, sector mix, and actual AI exposure.

A striking finding is the near-total absence of harm disclosures across five years of filings. Across 9,821 annual reports from more than 1,300 companies spanning 2020 to 2025, only nine harm-tagged chunks were identified — a rate of effectively zero. UK listed companies rarely disclose realised AI harms in their annual reports. This is itself a signal: either AI-related harms have not yet materialised in ways that boards feel obliged to disclose, or — more plausibly — the annual report format systematically suppresses harm acknowledgement in favour of risk framing. Either way, annual reports alone are insufficient for harm surveillance; regulatory enforcement records, litigation filings, and incident databases are needed as complementary sources.

The Observatory's most important near-term function is as a pre-intervention baseline for Provision 29 of the 2024 UK Corporate Governance Code, which takes effect for FY2026. If the Code is working as intended, the next annual cohort should show improvement in disclosure specificity and governance depth, not just mention rates. Annual reports are a lagging instrument, but they are one of the most systematic and legally accountable evidence bases available for monitoring corporate AI governance at scale.

Appendix A: Classifier Definitions

This appendix reproduces the canonical label definitions used in production classification. These definitions are the operative specifications against which the golden set was annotated and against which classifier output was evaluated. Minor formatting differences from the production prompt YAML have been made for readability; no substantive content has been altered. For the exact prompts used see: github.com/84rt/ai-risk-observatory

A.1 Keyword Gate (Stage 1 Pre-filter)

Before any classification is attempted, a chunk must pass the following hard gate:

The excerpt must explicitly mention AI, ML, LLM, GenAI, or a clearly AI-specific technique such as machine learning, neural networks, or computer vision. Terms such as "data analytics," "automation," "digital tools," "advanced analytics," or "predictive tools" do not qualify as AI under this definition unless AI is explicitly named or a specific AI technique is unambiguously described.

Chunks that do not pass this gate are assigned none and do not enter Stage 2. This rule is the single most consequential boundary decision in the pipeline: it excludes a large class of adjacent technology language that prior studies have sometimes treated as proxies for AI activity.

A.2 Stage 1: Mention Type Labels

adoption: Describes real, current deployment, implementation, rollout, pilot, or use of AI by the company or for its clients. Requires company-specific language ("we," "our," "our clients"). Generic intent, strategy, roadmaps, or future plans do not qualify. Phrases such as "exploring," "piloting," or "investigating" qualify only when they refer to a specific initiative currently underway. Delivering AI systems to clients counts as adoption; pure consulting or advisory work without deployment does not.

risk: AI is described as a risk or material concern to the company: legal, cybersecurity, operational, reputational, or regulatory risk directly caused by or attributed to AI. The classifier must verify that AI is the named source of the risk. A passage that mentions a risk category in one sentence and AI in a separate, unconnected sentence does not qualify.

harm: AI is described as having caused a past, specific harm, such as: misinformation spread, fraud enabled by AI, safety incident, discriminatory outcome, or other. Harm is distinguished from risk (prospective) by its past tense or completed framing.

vendor: Explicit mention of a named third-party AI vendor or platform that provides AI technology to the company, or a named product that is clearly AI (e.g., GPT, Google Gemini, Microsoft Copilot). The emphasis is on what AI models or systems the company uses, not merely that a technology partnership exists.

general_ambiguous: AI is explicitly mentioned (satisfying the keyword gate) but the passage does not meet the threshold for any of the above labels. Typical examples: high-level strategy statements, board-level AI acknowledgements, industry trend commentary, or AI opportunity language without operational specificity.

none: No AI mention, a false positive (place name containing "ai," unrelated abbreviation, foreign language fragment), or automation/digital language that does not pass the keyword gate.

A.3 Stage 2a: Adoption Type Definitions

All three adoption types are non-mutually exclusive and each receives a signal score of 0–3.

non_llm (Traditional AI/ML): Everything that is AI but not LLM-based or agentic: computer vision, predictive analytics, fraud detection models, recommendation engines, anomaly detection, robotic process automation with ML components, natural language processing systems that predate the LLM era.

llm (Large Language Models and Generative AI): GPT, ChatGPT, Gemini, Claude, Copilot, text generation systems, NLP chatbots, document summarisation, code generation, and any system in the GenAI category. AI copilots and AI assistants default to llm unless explicitly described as operating autonomously.

agentic (Autonomous AI Systems): AI systems or agents that autonomously execute tasks and take actions with limited human oversight. The key characteristic is autonomous execution: the AI acts, decides, and operates on its own rather than assisting a human who decides.

Signal guidance (0–3): 0 = type not present; 1 = weak or implicit signal, type is plausible but not stated; 2 = strong implicit signal, type is clearly implied but not explicit; 3 = explicit and unambiguous mention.

A.4 Stage 2b: Risk Category Definitions

All ten categories are non-mutually exclusive. Each assigned category receives a signal score of 1–3. Assignment requires that AI is attributed as the source of the risk; generic risk language not linked to AI yields none.

| Category | Operational Definition |

|---|---|

strategic_competitive | AI changes market structure, customer behaviour, pricing power, or competitive position. Failure to adopt AI, competitive obsolescence, or industry disruption attributable to AI. |

operational_technical | AI quality, reliability, and model-risk issues. Model failures, accuracy problems, hallucinations, system instability, unsafe outputs, or decision-quality degradation caused by AI systems. |

cybersecurity | AI-linked attack or defence exposure. AI-enabled phishing/fraud/impersonation, adversarial attacks on AI systems, AI-accelerated data breaches, AI-enhanced social engineering. |

workforce_impacts | AI-driven workforce transition risk. Skills gaps caused by AI adoption, displacement pressure, retraining obligations, unsafe or unauthorised employee AI use (shadow AI). |

regulatory_compliance | AI-specific legal, regulatory, privacy, or IP exposure. EU AI Act compliance costs, GDPR/privacy implications of AI, IP and copyright risks from AI-generated content, legal liability from AI decisions, regulatory uncertainty. |

information_integrity | AI-enabled misinformation, deepfakes, content authenticity erosion, manipulation risk. The AI must be attributed as the mechanism producing or enabling false or manipulated content. |

reputational_ethical | AI-linked trust erosion, algorithmic bias, fairness concerns, ethical objections, or social licence risk. Covers both internal (employee) and external (public/investor) trust. |

third_party_supply_chain | Over-reliance on AI vendors, concentration risk from a small number of AI providers, downstream misuse of AI in the supply chain, or risks arising from third-party AI embedded in the company's products or services. |

environmental_impact | AI energy consumption, carbon footprint from training or inference, hardware resource intensity, and sustainability concerns attributable to AI use. |

national_security | AI-linked geopolitical or security instability, exposure of critical infrastructure to AI-enabled threats, export-control and security-of-state concerns, and AI in defence/intelligence contexts where national security implications are explicit. |

Signal guidance (1–3): 1 = weak implicit attribution, plausible but lightly supported; 2 = strong implicit attribution, clear with some interpretation; 3 = explicit attribution, AI is directly stated as the cause of that category risk.

A.5 Stage 2c: Substantiveness Definitions

The substantiveness scale applies separately to risk, adoption, and vendor chunks. The definitions are functionally similar but operationally distinct because the disclosure tasks differ.

Risk substantiveness:

boilerplate: Generic risk or governance language with little concrete mechanism. Could appear unchanged in any company's report (e.g., "AI poses risks to our business").moderate: Identifies a specific AI-risk area but provides limited mechanism or mitigation detail. The reader learns what risk area is relevant but not how the risk operates or what is being done about it (e.g., "AI regulation may affect our compliance obligations").substantive: Describes a specific AI-risk mechanism and provides concrete mitigation actions, operational commitments, named systems, or measurable targets (e.g., "We allocated £5M to reclassify three high-risk AI systems under the EU AI Act by Q3 2025").

Adoption substantiveness:

boilerplate: Pure jargon with no information content. Could appear in any company's report unchanged (e.g., "We leverage AI to drive innovation and improve operations").moderate: Identifies a specific use case or domain but lacks concrete detail (e.g., "We use AI in our underwriting process").substantive: Names specific systems, quantifies impact, or explains what/how/why with technical or operational detail (e.g., "We deployed GPT-4 for document review, reducing processing time by 40%").

Vendor substantiveness:

boilerplate: Generic reference to AI tools, technology providers, or external platforms without identifying a specific vendor or model (e.g., "We work with leading AI technology providers").moderate: Names a specific vendor, model, or platform but provides no use case, scale, or outcome (e.g., "We use Microsoft Copilot").substantive: Names a specific vendor, model, or platform and links it to a concrete use case, deployment context, scale, or outcome (e.g., "We use Azure OpenAI Service to power document summarisation for 8,000 employees").

A.6 Stage 2d: Vendor Tag Definitions

| Tag | Coverage |

|---|---|

microsoft | Microsoft Azure AI, Microsoft Copilot (all variants), Power Platform AI features, Bing/Search AI, and any Microsoft-branded AI product |

google | Google Gemini, Vertex AI, Google Cloud AI/ML APIs, DeepMind products deployed commercially, Google Workspace AI features |

openai | GPT series (GPT-3, GPT-4, GPT-4o), ChatGPT, DALL·E, Whisper, OpenAI API references |

amazon | AWS Bedrock, Amazon SageMaker, Amazon Rekognition, Amazon Comprehend, Amazon Lex, and other AWS AI/ML services |

nvidia | Nvidia DGX systems, NIM microservices, Nvidia AI Enterprise platform, Triton Inference Server, CUDA-based AI infrastructure |

meta | Llama series (Llama 2, Llama 3, Code Llama), Meta AI assistant, PyTorch where deployed as a production AI system |

salesforce | Salesforce Einstein AI, Agentforce, Sales Cloud AI, Service Cloud AI, and other Salesforce AI-integrated products |

ibm | IBM watsonx platform (watsonx.ai, watsonx.data, watsonx.governance), Watson AI services, IBM Cloud AI/ML services |

databricks | Databricks Mosaic AI, MLflow, Unity Catalog AI features, Databricks Lakehouse AI capabilities |

snowflake | Snowflake Cortex AI, Snowflake ML, Arctic foundation model, Snowflake AI Data Cloud features |

anthropic | Claude series (Claude 1, 2, 3, Haiku, Sonnet, Opus) |

xai | xAI Grok series (Grok-1, Grok-2), xAI API references |

palantir | Palantir AIP (Artificial Intelligence Platform), Foundry, Gotham, and other Palantir AI-integrated products |

arm | Arm Ethos NPUs, Arm Cortex AI compute, Arm AI development tools used as AI inference infrastructure |

mistral | Mistral AI models: Mistral series (Mistral 7B, Mistral Large), Mixtral series, Le Chat |

uk_ai | UK-headquartered AI providers not otherwise listed (e.g. Stability AI, BenevolentAI, Faculty AI) |

open_source_model | An open-source AI model deployed directly without a named commercial provider or hosted service (e.g. Llama deployed on-premises, Falcon, Mistral self-hosted) |

internal | Company explicitly describes building, training, or maintaining its own AI systems in-house or through a proprietary development programme |

other | A named AI provider or product that does not match any of the above tags (e.g. Scale AI, Cohere, Writer, Glean) |

undisclosed | An external AI capability or provider is referenced but not named (e.g., "our AI vendor", "third-party AI tools", "external AI platform") |

Multiple vendor tags may be assigned to a single chunk if more than one provider is named. The internal and undisclosed tags may co-occur with named-vendor tags only if the passage clearly refers to both.

Appendix B: Corpus Coverage and CNI Mapping

B.1 Coverage Summary

| Coverage item | Count / note |

|---|---|

| Starting LSE-listed company universe | 1,660 |

| Excluded non-UK or no Companies House registration | 191 |

| Target UK-incorporated universe | 1,469 |

| Companies with processed reports | 1,362 |

| Processed annual reports | 9,821 |

| Primary analysis window | 2021–2025 |

| Supplementary years | 2020 and partial 2026 |

| Known companies without FinancialReports.eu coverage | 178 |